IPEV 2025: What changed and why It matters for your quarterly valuation process

The updated IPEV Valuation Guidelines come into force for reporting periods beginning on or after 1 April 2026. This is not a cosmetic refresh. It is the most consequential tightening of valuation expectations in years for private market funds that report fair value to LPs. The core valuation principles remain intact, but the 2025 edition makes one thing much clearer: firms are expected to apply those principles with more discipline, more evidence, and far better documentation than many current quarterly processes can support.

The shift matters because a large part of the market still runs valuations through fragmented spreadsheets, static assumptions, manually rebuilt waterfalls, and lightly documented judgment calls. That is becoming much harder to defend. The 2025 Guidelines place sharper emphasis on calibration, complex capital structures, hybrid instruments, valuation governance, documentation, traceability, and the role of AI. They do not say that every fund needs an entirely new valuation philosophy. They do say, very clearly, that the process behind the number now has to stand up to far more scrutiny.

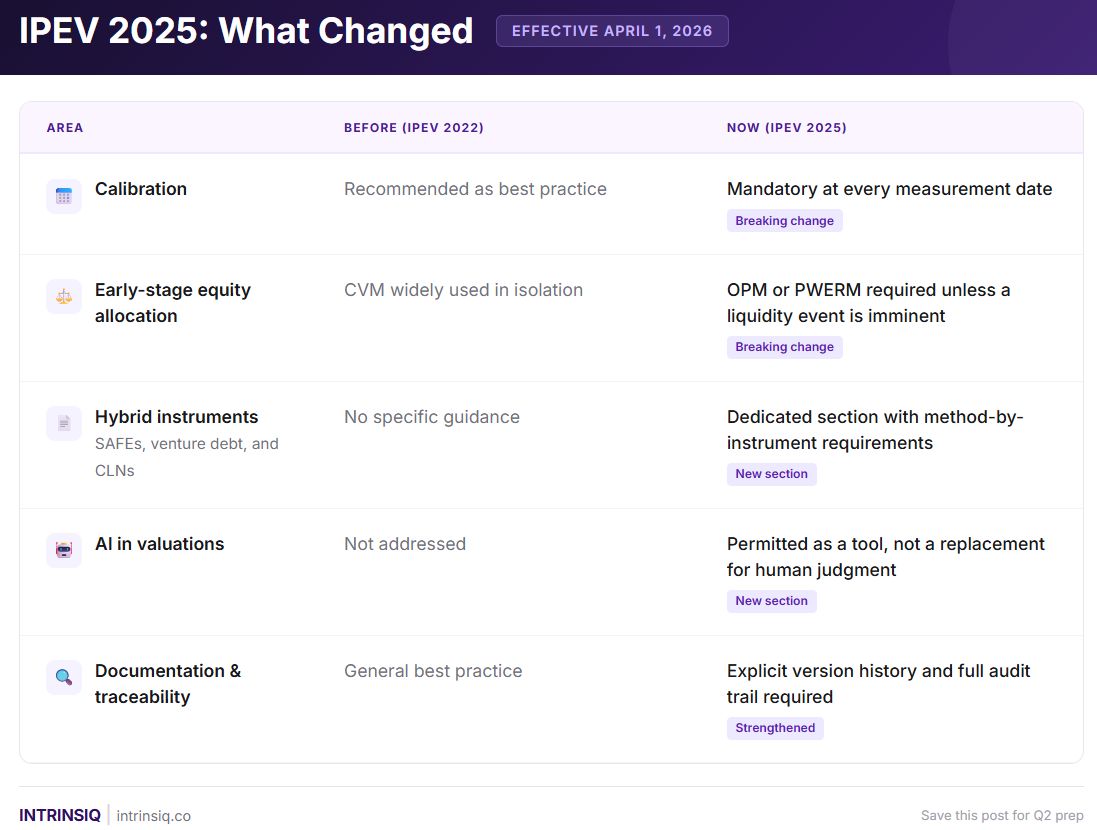

At a glance, these are the changes most likely to affect how private market funds run their quarterly valuation process.

What these changes mean in practice

The table above gives the headline view. The practical impact is where IPEV 2025 becomes real.

The Board deliberately preserved the historical framework of the Guidelines and focused on enhancing the explanatory text and expanding guidance in key areas. That matters because the message is not that the valuation rulebook has been rewritten. The message is that several areas that were previously handled too loosely are now addressed with much greater clarity. And once guidance becomes clearer, the room to rely on habit, simplification, or undocumented judgment gets smaller.

For most VC and growth investors, three changes matter most in practice.

First, calibration now has to be treated as a recurring quarterly discipline. The 2025 Guidelines explicitly reaffirm that Fair Value should be estimated at each Measurement Date, defined as each time fair value based NAV is reported to investors, and that calibration is required by accounting standards. In other words, a valuation process cannot simply remain anchored to cost, the last priced round, or the previous quarter’s output without showing how that value has been tested and rolled forward against updated company performance and market conditions. If your process cannot reproduce the original transaction logic and evidence how assumptions evolved over time, that is no longer a minor weakness. It is a valuation control gap.

Second, simplified early-stage allocation approaches are becoming much harder to defend on their own. The updated guidance expands discussion around complex capital structures, liquidation preferences, scenario analysis, and the need to select methodologies that reflect the actual economics of the instrument and likely outcomes. Market commentary on the 2025 edition consistently points in the same direction: where there is meaningful uncertainty, multiple securities, or non-trivial preference structures, simple allocation shortcuts are increasingly inadequate. For many venture and growth portfolios, that means firms must be ready to justify the use of option-based, scenario-based, or hybrid methods rather than relying on a basic waterfall in isolation.

Third, hybrid instruments now require explicit, instrument-specific modelling. The 2025 Guidelines introduce a dedicated section on hybrid instruments and make clear that a one-size-fits-all approach is no longer appropriate for instruments such as SAFEs, venture debt, and convertible loan notes. This is one of the clearest signals in the new edition. Holding these instruments at cost, or treating them with overly generic mechanics, is becoming much harder to justify. The legal features of the instrument now have to drive the valuation approach, and firms need to show that the selected method matches those features in a disciplined and repeatable way.

Two additional changes strengthen this shift even further.

AI is now explicitly addressed, but only as a tool. The updated Guidelines and market commentary are clear that AI and automated models may support the valuation process, but they do not replace professional judgment, scepticism, or human challenge. This is important because many firms are now experimenting with automation across data extraction, modelling support, and reporting workflows. The 2025 message is not “do not use AI.” It is “you remain responsible for the judgment.”

Documentation and traceability are no longer soft best-practice concepts. The 2025 update places stronger emphasis on valuation governance, documentation of significant judgments, explainability of valuation movements, reviewability, and a robust control framework. Inputs, assumptions, methodology choices, and changes over time must be clearly documented. That raises the standard not just for the valuation output, but for the operating process behind it.

Why this matters now

For many funds, the real issue is not whether they understand these concepts in theory. It is whether their current quarterly workflow can actually apply them under time pressure, across multiple companies, with consistency and auditability.

That is where the gap appears.

A spreadsheet-driven process can often handle a straightforward mark. It becomes much more fragile when teams need to calibrate consistently every quarter, support methodology choices across complex cap tables, model hybrid instruments appropriately, document scenario assumptions, and maintain clear version history and review trails. The technical expectation is rising, but the operational burden is rising with it.

This is also why the 2025 update matters even for firms that believe their valuations are broadly reasonable today. The question is no longer only whether the final number can be defended. The question is whether the full path to that number is repeatable, transparent, and capable of withstanding scrutiny from auditors, LPs, internal finance teams, and valuation committees quarter after quarter.

What funds should be asking themselves

As 1 April 2026 approaches, private market funds should be asking some direct questions:

- Can we clearly show how our current quarter marks were calibrated from entry or from the prior measurement date?

- Can we defend where we still rely on simplified early-stage allocation logic?

- Do our methods for SAFEs, venture debt, and convertibles reflect the actual legal and economic features of each instrument?

- Can we evidence the assumptions, version history, reviewer challenge, and audit trail behind every significant judgment?

If the honest answer to any of these questions is “not consistently,” the issue is not just methodology. It is process design.

How Intrinsiq helps

Intrinsiq helps private market investors run a more structured, repeatable, and audit-ready quarterly valuation workflow.

Funds such as Highland Europe and Felix Capital use Intrinsiq to support quarterly valuations with stronger calibration discipline, robust treatment of complex capital structures, clearer documentation, and full traceability across assumptions and outputs.

With Intrinsiq, valuation teams can:

- run calibrated quarterly valuations across the portfolio,

- model complex waterfalls, preferences, convertibles, options, and carve-outs,

- support CVM, OPM, and PWERM outputs where appropriate,

- maintain a clear version history and audit trail,

- and produce valuation work that is easier to review internally and defend externally.

The value is not just speed. It is control. As IPEV 2025 raises the practical bar, that control becomes harder to treat as optional.

A practical next step

If you are unsure whether your current valuation process is ready for the updated IPEV expectations, the most useful next step is usually a gap assessment.

We are offering a complimentary 30-minute review of your current valuation workflow to help identify where the main pressure points may be under IPEV 2025.

No pitch. Just practical guidance on:

- calibration at each measurement date,

- where simplified allocation methods may no longer be sufficient,

- treatment of hybrid instruments,

- documentation and traceability gaps,

- and what auditors are most likely to challenge first.

.jpg)