How Felix Capital handles complex waterfall calculations every quarter

For private market investors, complex waterfall calculations are one of the hardest parts of the quarterly valuation process. The challenge is not simply getting to an answer once. It is getting to the answer repeatedly, under quarter-end pressure, in a way that is consistent, reviewable, and defensible.

That is exactly why firms like Felix Capital use a more structured workflow for handling complex waterfall calculations every quarter.

Why this matters every quarter

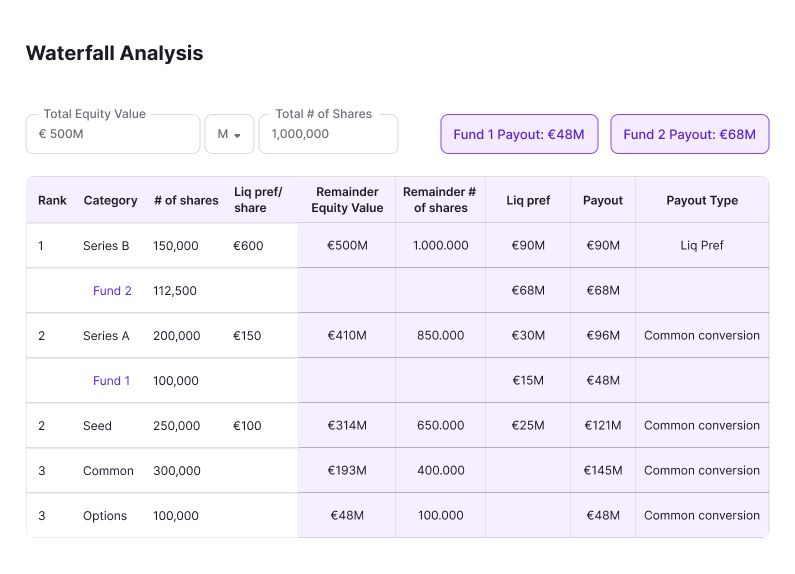

Waterfall calculations sit at the point where valuation theory meets real-world cap table complexity. A firm may have a clear view on enterprise value, solid market inputs, and a reasonable valuation methodology. But once that value needs to be allocated across multiple share classes, liquidation preferences, convertibles, options, carve-outs, management participation, and different outcome scenarios, the process becomes much more difficult to manage cleanly.

This is not limited to venture and growth funds. It also matters for buyout firms and other private capital investors dealing with management equity, ratchets, carve-outs, debt-like features, contractual rights, or structured instruments. The form of complexity differs by strategy, but the underlying issue is the same: once value has to be allocated through a non-trivial structure, the mechanics need to be robust, supportable, and clearly documented. The IPEV Guidelines are expressly intended to apply across the full range of private capital investments and to all debt and equity investments of investment entities.

Why complex waterfalls create such a persistent problem

Complex waterfalls are difficult because they are not just calculation exercises. They are control exercises.

A single case may involve:

- multiple liquidation preference structures,

- participating and non-participating preferred shares,

- convertibles,

- SAFEs or similar instruments,

- warrants and options,

- carve-outs,

- management incentive arrangements,

- and multiple plausible exit scenarios.

Each of those features affects how value is allocated. As the structure becomes more layered, the process becomes harder to model, harder to update, and harder to review. A model that technically works can still be operationally fragile if only one person understands how it works or if each quarter requires manual rebuilding.

That is where spreadsheets often start to break down. Not because they cannot produce a number, but because they struggle to produce a number in a way that is consistently traceable across quarters.

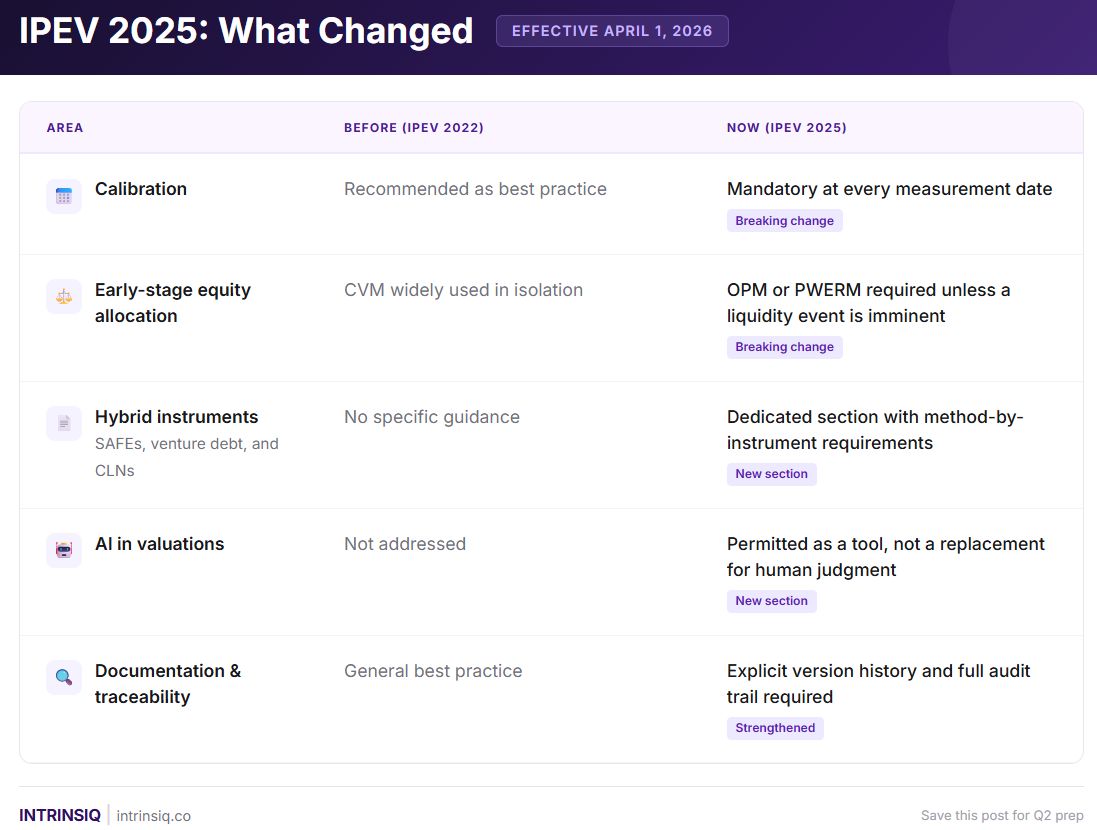

Why this matters more under the updated IPEV Guidelines

The updated IPEV Valuation Guidelines raise the practical bar for how private market firms need to handle this complexity. The historical framework has been maintained, but the 2025 edition materially expands explanatory guidance in areas that matter directly for complex waterfall calculations, including calibration, complex capital structures, hybrid instruments, documentation, process rigor, and the use of AI. The Guidelines also explicitly state that Fair Value should be estimated at each Measurement Date and that the Guidelines encourage consistency of methodology, appropriateness of valuation judgments, calibration of valuation inputs, and rigor in the valuation approach.

You can find the updated Guidelines here: IPEV Valuation Guidelines 2025.

The practical implication is straightforward. Complex waterfalls can no longer be treated as a side exercise in Excel that is lightly updated at quarter-end. Where a capital structure includes meaningful preferences, optionality, convertibles, carve-outs, management participation, or scenario-dependent outcomes, the allocation mechanics become part of whether the overall valuation is actually defensible.

What changed, and why it affects waterfalls

Several parts of the updated Guidelines matter directly here.

First, calibration must be treated as a recurring discipline. The updated Guidelines reaffirm that Fair Value should be estimated at each Measurement Date and emphasize calibrated valuation inputs as a core principle. That means firms cannot simply anchor to a historical output without being able to explain how assumptions and value have evolved over time.

Second, the 2025 edition adds more guidance around complex capital structures and mathematical models, which is directly relevant to how equity value is allocated through a waterfall. That matters because once a structure contains multiple securities with different rights, the allocation method becomes a substantive part of the valuation, not a mechanical afterthought.

Third, the Guidelines add specific discussion around venture debt and convertible instruments and include a dedicated focus on hybrid instruments. That raises the standard for how firms treat instruments whose economics are not captured well by simplistic shortcuts or static carrying values.

Fourth, the updated Guidelines explicitly address AI. They are clear that AI can support the valuation process, but cannot replace professional judgment and skepticism. The valuer remains fully accountable for the inputs, process, and conclusions. That is important in the context of waterfall automation: automation is useful only if the underlying logic remains transparent, deterministic, and reviewable.

Finally, the Guidelines place strong emphasis on documentation, challenge, governance, and control frameworks. The rationale for significant judgments should be documented, key assumptions should be challenged appropriately, and firms should have processes that support transparency and reviewability. That shifts the standard from “we have a model” to “we can explain, evidence, and defend the process behind the model.”

Does this relate to OPM and PWERM?

Yes, directly.

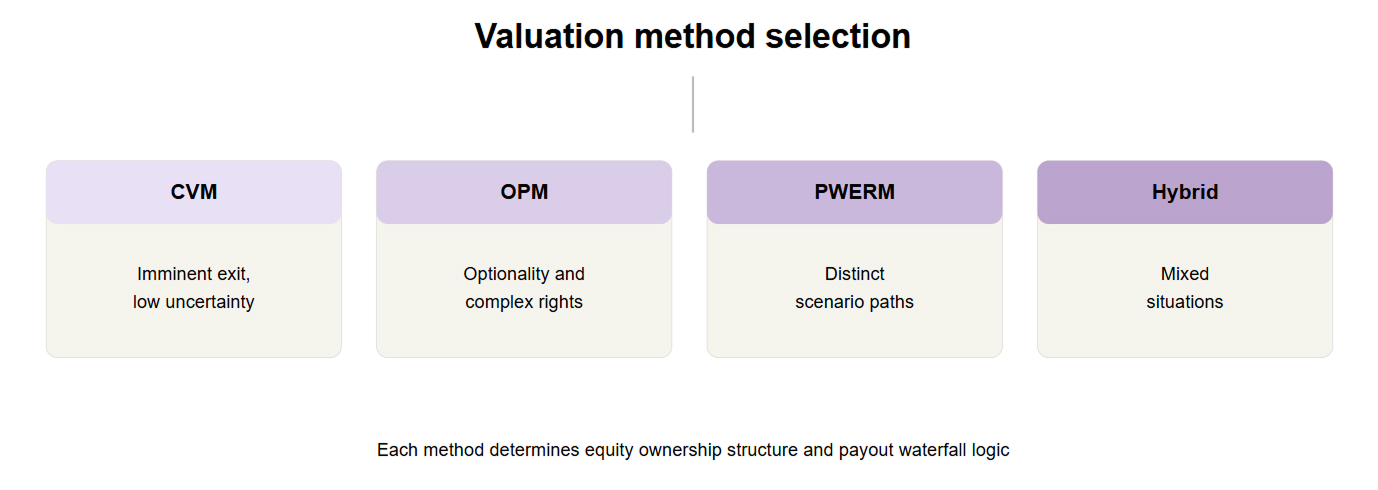

When people talk about “doing the waterfall,” they often mean the broader problem of allocating value correctly through a complex capital structure. Under the updated Guidelines, that question is closely linked to the choice of allocation method. Depending on the facts and circumstances, firms may need to support an approach such as CVM, OPM, PWERM, or a hybrid method.

The key point is that these are not separate issues. The waterfall mechanics and the choice of method are intertwined. If an exit is imminent, a simpler current-value allocation may sometimes still be appropriate. But where there is real uncertainty, optionality in outcomes, or multiple securities with different rights, firms increasingly need a more robust framework for allocating value. In practice, that is why methods such as OPM, PWERM, or hybrid approaches become so important in the context of complex waterfalls. The updated Guidelines’ expanded discussion of complex capital structures, mathematical models, and scenario-related applications reinforces this link.

How Felix Capital uses Intrinsiq

Felix Capital uses Intrinsiq to handle complex waterfall calculations as part of a more structured quarterly valuation workflow.

Instead of relying solely on manually maintained spreadsheets for the most difficult allocation cases, Intrinsiq helps bring the process into a system that supports:

- multiple liquidation preference types,

- convertibles,

- options,

- carve-outs,

- and different output methods, including CVM, OPM, and scenario-based approaches such as PWERM.

AI helps structure the model, while the calculations themselves remain fully deterministic.

That distinction matters. In valuation workflows, automation adds value only if the underlying math remains stable, transparent, and reviewable. The goal is not to replace rigor. It is to make rigor scalable.

When this becomes especially relevant

This kind of workflow becomes especially valuable when:

- quarter-end reporting is becoming too dependent on spreadsheet specialists,

- portfolio companies or investments have increasingly complex financing histories,

- the capital structure has become too complex for lightweight spreadsheet updates,

- reviewers need better documentation and traceability,

- or auditors are asking more detailed questions around methodology and assumptions.

For firms such as Felix Capital or Highland Europe, the complexity is often especially high because of multi-round financing histories, preference stacks, convertibles, and option-heavy cap tables. But the same underlying issue can arise in private equity when there are carve-outs, management participation, structured terms, or other rights that materially affect value allocation.

What changes operationally

A more structured workflow changes more than the calculation itself.

It helps teams move from:

- fragmented files,

- manual rework,

- opaque assumptions,

- and person-dependent logic

to:

- structured inputs,

- deterministic calculations,

- clearer outputs,

- and better traceability across quarters.

That matters because under the updated Guidelines, the pressure is not only on the final mark. It is on the repeatability and defensibility of the full process behind the mark. The Guidelines explicitly note the need for rigor, thoughtful valuation approaches, documented significant judgments, and strong control frameworks.

Why this matters now

As of 1 April 2026, the updated IPEV Guidelines are in effect for quarterly reporting periods beginning on or after that date. Firms that are still managing complex waterfalls primarily through fragile spreadsheets are likely to feel more pressure, not less. The question is no longer only whether the final number looks reasonable. The question is whether the full path to that number is robust, explainable, and capable of standing up to review quarter after quarter.

That is why firms like Felix Capital use Intrinsiq: not simply to calculate waterfalls faster, but to handle complex waterfall calculations every quarter in a more structured and reliable way.

A practical next step

If your team is still handling complex waterfall calculations primarily in spreadsheets, this is a good moment to review whether that process is still fit for purpose under the updated IPEV expectations.

We offer a complimentary 30-minute review of your current valuation workflow and can help identify where the main pressure points are, particularly around:

- complex cap table allocation,

- choice of allocation method,

- hybrid instruments,

- documentation and traceability,

- and repeatability across quarters.

No pitch. Just practical guidance.

.jpg)